Personal insolvency demographics: Headline rate hides large variations

07 August 2019

The Insolvency Service’s statistics on personal insolvency and demographics data always make for fascinating and sobering reading. The latest set, breaking down 2018’s individual insolvencies in England and Wales by age, gender, and location of the person becoming insolvent, is no exception, as the structural inequalities which affect people’s finances are laid bare.

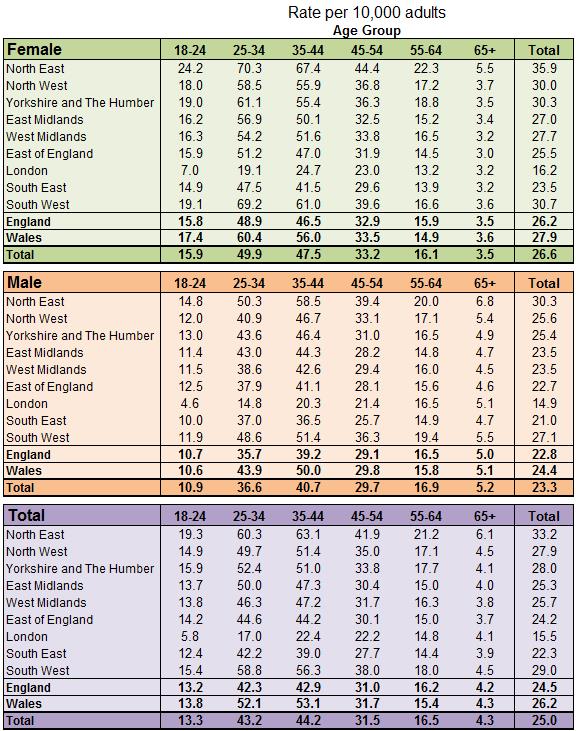

Since 2013, the rate of women becoming insolvent has been higher than the men’s rate; last year, 26.6 per 10,000 women entered insolvency, against 23.3 per 10,000 men (giving an average for all genders of 25 per 10,000 adults in England and Wales – or one in every 400 people). But this headline gender rate hides large variations, depending on the age and location of the person in question. For example, women aged 25-34 who live in the North East have an insolvency rate of 70.3 per 10,000, while women aged over 65 who live in the East of England have a rate of just 3 per 10,000 – over 23 times lower. For men, meanwhile, the group with the highest rate of personal insolvency is men aged 35-44 who live in the North East, at 58.5 per 10,000, while the lowest group is men aged over 65 in the West Midlands, with a rate of 4.5 per 10,000 – 13 times lower.

Rate of Individual Insolvencies in England and Wales, 2018

Source: The Insolvency Service

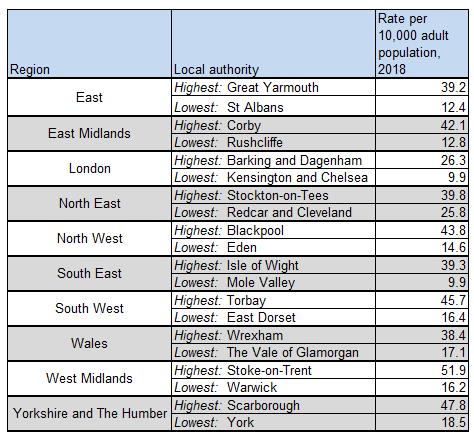

R3’s comments on the gender and regional disparities highlighted by the figures give a bit more background on the wider forces in effect which could lead to such a sharp difference in insolvency rates. And looking at variations within regions, at the local authority level, further emphasises the variations between different areas, even when they are not all that far apart, geographically speaking. The table below shows the local authorities for the 10 regions of England and Wales with the highest and lowest personal insolvency rates in 2018:

Local Authorities in each region of England/Wales with the highest and lowest rates of personal insolvency, 2018

Source: The Insolvency Service

You can check the rates of personal insolvency (Individual Voluntary Arrangements, Debt Relief Orders, and bankruptcies) for any local authority using this handy tool – just type in the name of the LA you’re looking for in the “Select local authority area” box.

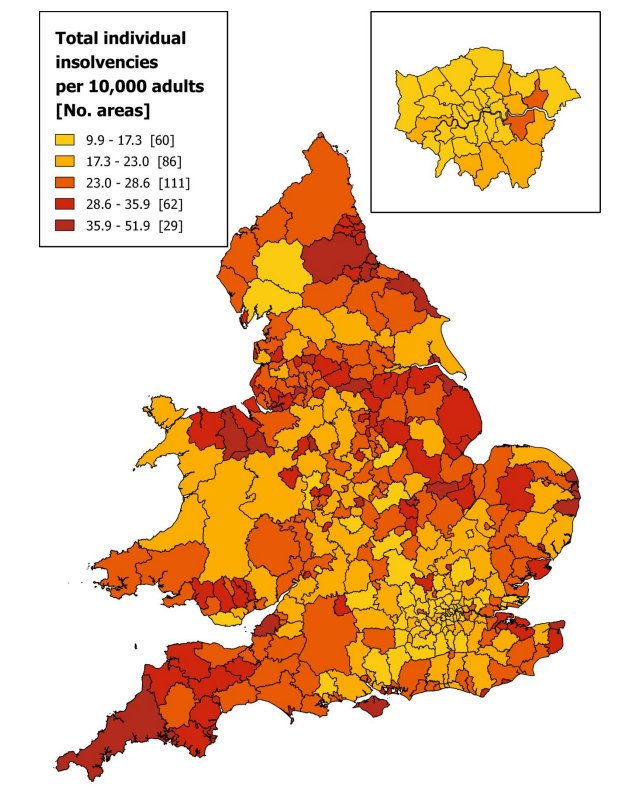

The Insolvency Service’s ‘heatmap’ is an excellent illustration of the tapestry of different personal insolvency rates across the country (a darker red indicates a local authority with a higher personal insolvency rate):

The difference in rates between the local authorities in the same regions with the highest and lowest rates illustrates the need to target interventions for people in debt carefully, to ensure the people who need it most are able to access help and support. It is also striking that the heatmap looks very similar to last year’s (and to 2014’s). The factors R3 has identified as contributing to higher levels of personal insolvency – such as the insecure nature of seasonal work in many coastal areas, and the deprivation caused by factory closures in post-industrial areas – are not phenomena which can be ‘solved’ overnight.

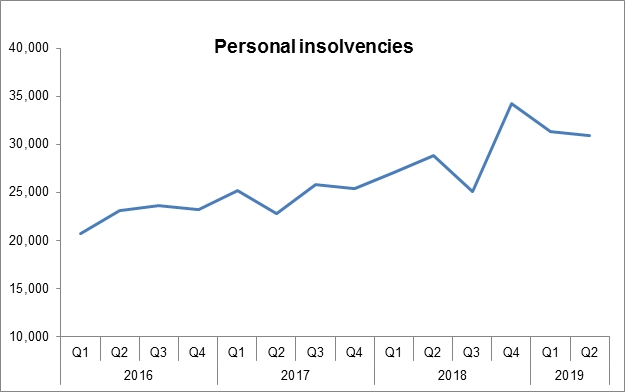

Meanwhile, the personal insolvency statistics from the Insolvency Service for Q2 2019 (England and Wales) showed that, for the second quarter in a row, the number of personal insolvencies decreased. However, personal insolvency numbers are higher than they were in the same quarter last year (up by over 7%), and are considerably above the level of Q2 2016 (when they were 35% lower than in the most recent set of figures).

Personal insolvencies (seasonally adjusted), England and Wales, Q1 2016 – Q2 2019:

Source: The Insolvency Service

Personal insolvency can represent a fresh start to many people – an opportunity to resolve financial problems and move on, with luck to a more stable footing for the future. With personal insolvency numbers generally higher than they were a few years ago, people who are worried about their debts should take action, by seeking help and advice from a qualified and professional source. As the personal insolvency demographics data show, people of all ages and genders, and living in all parts of the country can be affected – but seeking advice, preferably before matters spiral out of control, is always a good first step.

Dawn Boyall

Dawn Boyall Amani Keynan

Amani KeynanR3 members can provide advice on a range of business and personal finance issues. To find an R3 member who can help you, click below.