Navigating an uncertain macroeconomic environment

08 September 2022

Unlike initial predictions, 2022 has (so far) been a year of growth deceleration and high inflation. And as UK retail prices hit the highest rate of inflation since 2008 and the Russia-Ukraine war wages on, supply chains are facing further pressure – impacting the growth of businesses in the process.

In fact, in May’s Dun & Bradstreet’s Global Business Risk Report, supply chain disruption is identified as the most pressing of the top ten issues for the global risk environment for the second quarter of 2022, with the Russia-Ukraine war and China’s Covid-19 strategy adding pressure on already strained production chains.

But how are these crises affecting supply chains, and how can actionable data and insights help to mitigate risks and enable businesses to thrive during times of volatility and uncertainty?

The Covid Legacy

Almost all (99%) procurement and supply chain leaders across a range of industries surveyed in the UK and US say that Covid-19-related economic disruption had an impact on their supply chain operations. Some of the ways this has manifested include:

1. Operational inefficiency: As the pandemic impacted business operations, companies had to race to digitally transform to move their business online to continue trading. But not every business had the capacity to adapt at pace.

2. Staff shortages: With soaring resignations across the country, many sectors across the UK are experiencing staff shortages – with haulage, food and drink, hospitality, and construction the hardest hit. According to the ONS, the number of job vacancies in April to June 2022 was 1,294,000. This was an increase of 6,900 from the previous quarter and an increase of 498,400 from before the pandemic in January to March 2020.

3. China’s economic slowdown: The intermittent closure of ports and factories in China to stamp out the spread of Covid-19 continues to impact supply chains across the world, extending goods and commodities shortages. This reduces lead times predictability and keeps prices elevated, which consumers ultimately bear the brunt of.

The slow-burn impact of Brexit

The EU is the UK’s largest trading partner, accounting for 54% of imports and 49% of exports of goods, making Brexit a great concern for companies with UK operations.

Worry and uncertainty has impacted businesses since the UK announced the Brexit vote in 2016, possibly contributing to reduced business investment and productivity. However, and perhaps surprisingly, in the years following the referendum, the impact of Brexit on trade has been limited, at least until the Trade and Cooperation Agreement (TCA) entered into force.

While it might be too soon to draw conclusions on the long-term effects of Brexit on trade, it’s clear that the TCA is no substitute for free trade, as it failed to address the significant regulatory, logistical, and administrative barriers to trade. And this has impacted most businesses, particularly small and medium-sized businesses who are feeling the pressures of the non-tariff barriers.

Organisations with higher levels of trade, employment, regulatory and ownership links with the EU also report significantly more Brexit-related uncertainty. Not to mention the rising costs of goods and services we’re currently experiencing due to inflation, which could in part be attributed to Brexit, a source of uncertainty for supply chains that adds to existing volatility and vulnerability in the supply chains of many industries.

Challenges due to the Russia-Ukraine war

The war between Russia and Ukraine has led to sanctions being imposed on Russia, and as access to oil, gas, electronic chips, and other products continues to decline, the supply chain of businesses across the globe remains under stress.

In addition, the disruption to supplies is leading goods exporters in Asia, Africa, and Latin America to impose and persist with their own export and price controls, which is also likely to affect inflation rates at a time when de-globalisation forces seem to gain momentum.

However, reorganising supply chains on a global scale is bound to add inflationary pressure and the future remains uncertain. And in the meantime, organisations exposed to international markets could see an increase in credit risk due to the challenges caused by the Russia-Ukraine conflict.

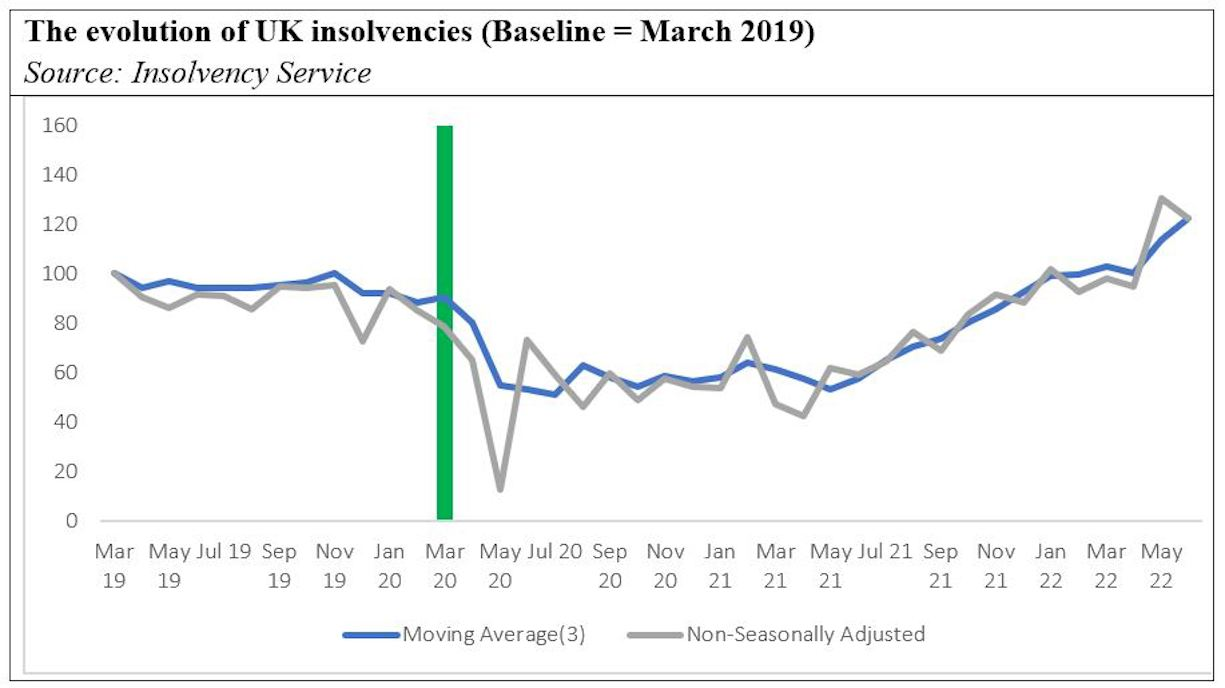

The insolvencies bill

In 2020 and 2021, the pandemic and the related support packages that followed froze the normal functioning of credit markets. Businesses could rely on a flood of cheap liquidity that led creditors to extend their liquidity runway in the hope of outrunning the pandemic.

As the tide turns, many businesses, especially those that have taken on additional debt and have not made operational transformation or strategic realignments for the post-pandemic era, may find themselves in the midst of a very real crisis in 2022.

The chart below shows that growth in UK company insolvencies has accelerated significantly in the second half of 2021, with the number of insolvencies now more than 20% higher than in March 2019.

Today’s trade landscape is impacted by a series of shocks, from the war in Ukraine, ongoing ramifications of Covid-19, Brexit trade barriers, to global supply challenges.

Unlike initial predictions, 2022 has (so far) been a year of growth deceleration and high inflation. And as UK retail prices hit the highest rate of inflation since 2008 and the Russia-Ukraine war wages on, supply chains are facing further pressure – impacting the growth of businesses in the process.

Yet, amidst all the chaos, organisations must still find a way to keep operations moving. So, business leaders need the right tools and systems to navigate the increasingly complex global supply chains with accurate supplier data and advanced analytics.

The UK’s economy has been forecast to go from the second-fastest growing economy in the G7 group of industrial nations (UK, US, Canada, Germany, Japan, France and Italy) to the slowest growing by 2023. Also, the likelihood of seeing a recession in major economies like the US, the Euro area, and the UK by the end of 2022 or in 2023 has increased significantly.

So, as the year continues to play out, businesses would benefit from the implementation of a strategy where risk is assessed holistically.

This is where data can provide firms with an informational advantage. After all, data is information on a phenomenon (for example one whose roots are only partly understood) or business of interest.

Somewhat unsurprisingly, two-thirds (67%) of UK business leaders now feel data is now an integral part of supply chain monitoring. This is likely to help them in at least two ways.

First, the collected information can increase agility and thus facilitate adaption to shocks, possibly helping businesses to turn risk into opportunities. Second, it can be used to increase efficiency, by shedding light on where costs should be cut, or investments be made.

Through this data-driven, risk-based approach, businesses will enable them to assess any potential impact and identify new opportunities – ensuring their business continuity as nations across the globe weather this present economic storm.

So, as the year continues to play out, businesses would benefit from the implementation of a strategy where risk is assessed holistically.

Tommaso Aquilante is associate director of economic research at Dun & Bradstreet.