Young people and personal insolvency: Rates creeping upwards

28 August 2019

- See our previous post on personal insolvency demographics here

Between 2015 and 2018, the rate of young people (aged 18-24) entering a form of personal insolvency rose by 110%, while the number of personal insolvency cases among under 25s rose by 104%. Over the same period, the rate of personal insolvencies for people of all ages rose by 42%, and the total number of cases rose by 45%.

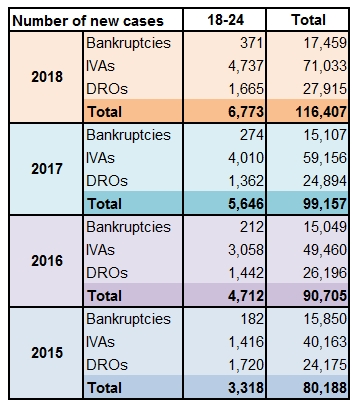

The increase in young people entering an insolvency procedure (an Individual Voluntary Arrangement, a Debt Relief Order, or bankruptcy) over just four years is certainly eye-catching, and a few media outlets picked up on the rise. However, it’s important to put the figures into context: the number of personal insolvency cases among under-25s rose from 3,318 in 2015 to 6,773 in 2018, while total personal insolvencies for people of all ages grew from 80,188 to 116,407. Under-25s made up 4% of personal insolvencies in 2015, and 6% in 2018 – a rising proportion, to be sure, but one that is still far outweighed by other age groups (in 2015, those aged 35-44 made up the largest percentage of personal insolvency cases, at 28.7%; in 2018, the 25-34s had the highest proportion of personal insolvencies, at 31.4% of the total).

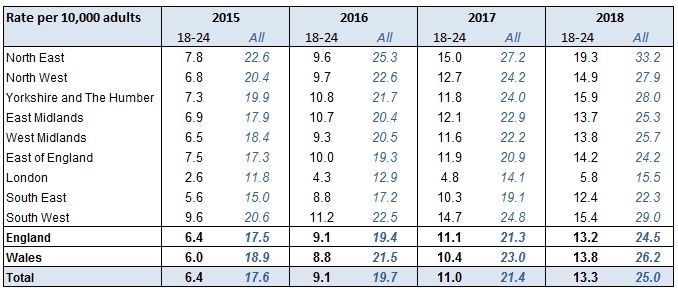

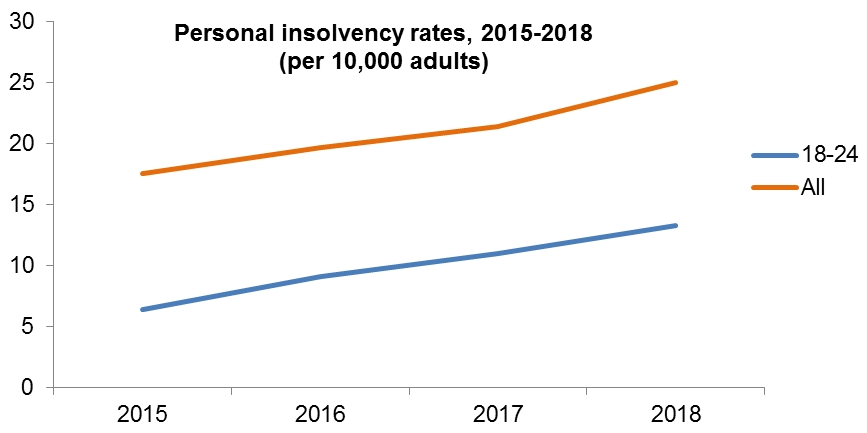

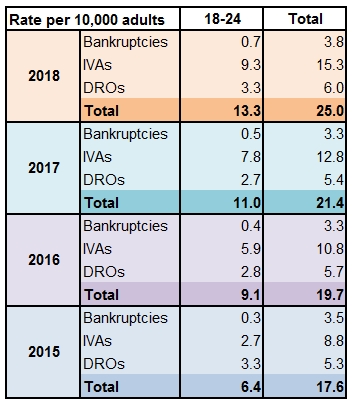

Looking at the rates gives a similar picture: while going from a personal insolvency rate of 6.4 per 10,000 18-24 year olds in 2015 to 13.3 in 2018 is a big jump, more than doubling over four years, the rate for under 25s is still lower than for all adults (17.6 per 10,000 adults in 2015; 25.0 per 10,000 in 2018). It is fair to say, though, that there is cause for some concern: the rate for 18-24 year olds has risen from being 36% as high as the all-adults rate in 2015 to being 53% as high in 2018. The rate for this age group also differed depending on region, from just 5.8 per 10,000 of those aged 18-24 in London, to 19.3 per 10,000 in the North East – over three times higher.

Source: The Insolvency Service/R3

What is driving this trend among young people? We don’t tend to associate young people just starting their adult lives with unmanageable debt issues; the type of debt most usually associated with young people in the 18-24 age bracket is student loans, which do not have to be repaid until the borrower is earning more than a certain threshold, with payments rising in line with income – keeping them theoretically affordable. It’s also worth remembering that student loans can’t be written off as part of an insolvency procedure, so they won’t be a direct cause of insolvencies. However, for young people who have started off in a new job and who are earning over the threshold for repayments, a student loan will be yet another source of pressure on their budgets, and may contribute to financial worries.

Many in this age group do not have a student loan, of course – but they may well have other debts. R3’s Personal Debt Snapshot research, from March 2019, found that 46% of British adults aged 18-24 said they are worried about their current level of debt (all ages: 40%). Of those British adults aged 18-24 who said they are worried about their current level of debt, student loans were cited by 57% as a cause of debt worries, followed by overdrafts (23%) and credit cards (21%).1

A lot of 18-24 year olds will still live with their families, with lower rents (or no rent at all), but a sizeable minority are in private rented accommodation (11.5% of private sector renters were people aged 16-24 in 2017, according to the ONS). Young people who are just starting out in their careers, or who are employed through zero hours contracts, are likely to be on lower pay than other age groups, and thus have less financial headroom, and less ability to build up savings.

Between the ages of 18 and 24 is when most people will become financially independent for the first time: leaving education, getting first full-time jobs, and applying for their first credit products. Accessing consumer credit products – such as personal loans, credit cards, car finance, overdrafts, and mortgages – is a normal part of adult life, but taking out finance can feel like a large step for a first-timer. In an ideal world, all school leavers would have had a comprehensive and practical course of financial education, to give them a thorough grounding in how debt, interest rates, and common financial products work – but, as R3’s research from 2017 found, a third (32%) of British adults aged 18-24 said they had never received advice on how to manage their personal finances through their school or university. Even among those who had received financial education via their place of education, what they were taught may not have been sufficient to prepare them for taking responsibility for their own budgets: among British adults of all ages, our research found that just one in ten (10%) rated the advice they received about personal finance through their school or college as useful.* Although it is unlikely by itself to be a leading cause of insolvency among young people, a low level of financial literacy certainly is not helpful.2

The internet literacy of young people, by contrast, may be one reason why the personal insolvency rate among 18-24s has increased in recent years, as young people with debt worries turn to a search engine for answers, and are able to access sites explaining different options for dealing with debt, including insolvency. Since 2016, it has been possible to apply to become bankrupt online, which may have improved the visibility of personal insolvency in general for young people: the statistics from the Insolvency Service show that bankruptcy numbers among 18-24 year olds have risen since 2015, although bankruptcy is still by far the least-frequently utilised form of personal insolvency for this age group (and, indeed, for all age groups).

Source: The Insolvency Service/R3

The sharpest growth for 18-24s has been in IVAs – up by 235% in numbers and 244% in rates between 2015 and 2018. IVAs are usually associated with consumer debt, and may be a sensible option for young people with assets, income levels and debts above the thresholds set for DROs. Google results for ‘debt advice’ and related searches often point people towards an IVA, which may partly explain why more young people are opting for an IVA.

A personal insolvency procedure will stay on someone’s credit history for six years, following completion or discharge from the procedure; this may be less of a burden to bear for young people who are likely to have less immediate need for credit than other age groups, on average. Their relative youth also means 18-24 year olds who become insolvent will have a longer time to rebuild their credit rating after going through an insolvency process before applying for a major credit commitment, such as a mortgage.

Overall, the growth in numbers and rates of under-25s who become insolvent over the past few years is notable. While still lower than other age groups, the increases for 18-24s have been greater than the all-ages trend. Insolvency can be a useful route to a financial fresh start, for people of any age, but support should be targeted at this age group, to help them find the best possible option for their financial situation.

*Rating it as 7-10 on a 0-10 scale where 0 = not useful at all and 10 = very useful

1. ComRes interviewed 2,004 British adults online between the 29th and 31th of March 2019. Data were weighted to be demographically representative of all British adults. ComRes is a member of the British Polling Council and abides by its rules. Full data tables are available at www.comresglobal.com.

2. ComRes interviewed 2,045 British adults online between the 1st and 2nd February 2017. Data were weighted to be demographically representative of all British adults. ComRes is a member of the British Polling Council and abides by its rules. Full data tables are available at www.comresglobal.com.

Stuart McBride

Stuart McBride Amelia Franklin

Amelia Franklin Lyle Horne

Lyle HorneR3 members can provide advice on a range of business and personal finance issues. To find an R3 member who can help you, click below.